A cell phone and landline both are phones that help you communicate. But cell phones give you a lot of flexibility in terms of portability, utility, etc. Likewise, flexi cap funds and multi cap funds both are equity mutual funds, but flexi cap funds offer more flexibility.

To understand flexi cap vs multi cap, you must first know about the classification of companies based on market capitalisation. As such, there are three types of companies – large cap, mid cap and small cap. Investments in large cap companies help with stability and capital protection, whereas investments in small cap and mid cap companies offer the potential for capital appreciation. While multi cap funds must invest in all three market cap segments, flexi-cap funds have a choice. Let’s understand how.

What are multi cap funds?

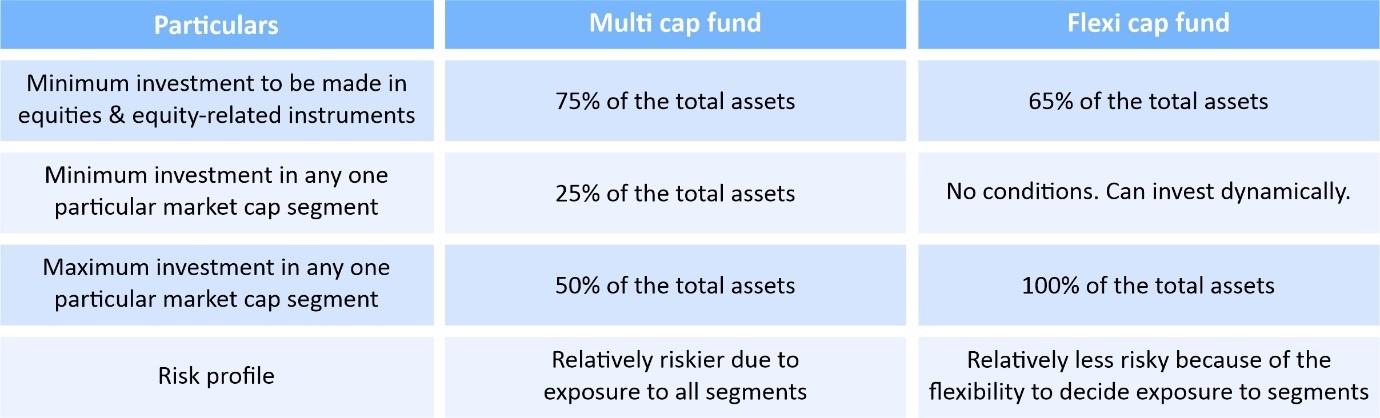

A multi cap fund must invest a minimum of 75% in equities and equity-related instruments such that at least 25% of the corpus is invested in large cap, mid cap and small cap companies each. Yes, such mutual fund schemes have the liberty to increase the maximum investment to a particular segment to 50% in order to make the most of market opportunities. But there is also a restriction – they can’t reduce their exposure to a particular segment below 25% even if the market conditions are bad.

What are flexi cap funds?

To help investors overcome the challenges faced by multi cap funds, the Securities and Exchange Board of India (SEBI) introduced flexi cap funds. Such funds must invest a minimum of 65% in equities and equity-related investments. But it is not mandatory for them to invest a minimum of 25% in any particular market cap segment. Instead, they have the liberty to invest dynamically across market capitalisations.

Flexi cap vs multi cap fund – Points of difference

Taxation of multi cap funds and flexi cap funds

Since both these funds have at least 65% of the corpus invested in equities and equity-related securities, they are equity-oriented funds and will be taxed similarly. The amount of tax you will pay on redemption will depend on how long you stayed invested in the fund. If you stayed invested for a year or less, your gains on redemption will attract a 15% short-term capital gains tax. If you stay invested for more than a year, your gains in excess of Rs. 1 lakh/year will attract a 10% long-term capital gains tax. Long-term capital gains up to Rs. 1 lakh/year are tax-free.

To sum it up

Just like large cap funds, mid cap funds and small cap funds, multi cap funds and flexi cap funds too are equity funds. While choosing between the two, you must assess your investment objective. But most importantly, you must assess your risk appetite. As opposed to multi cap funds, flexi cap funds can help you navigate market volatility with more flexibility. So, decide accordingly.

An investor education initiative by Edelweiss Mutual Fund

All Mutual Fund Investors have to go through a onetime KYC process. Investor should deal only with Registered Mutual Fund (RMF). For more info on KYC, RMF and procedure to lodge/redress any complaints, visit - https://www.edelweissmf.com/kyc-norms

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATEDDOCUMENTS CAREFULLY

Trending Articles

Signup for our Newsletter

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.